After both gold and silver recorded all-time highs on Thursday, January 29, 2026, at USD 5,598 and USD 121.65 respectively, prices of both metals declined sharply. Gold prices fell by around 21% from the peak to the low recorded yesterday at USD 4,403, indicating that the yellow metal has officially entered a bear market. However, the USD 4,400 level has proven to be a strong and resilient support, as gold failed to break below it or sustain trading beneath this area. This led to a strong rebound, with prices rising by around 9% from the low to current levels, above USD 4,800.

As for silver, prices declined by approximately 41% from the peak to the low recorded yesterday at USD 71.38, meaning that the white metal has also officially entered a bear market. Levels around USD 71–70 appear to be strong support zones that silver prices have so far failed to break. However, unlike gold, silver remains within the bear market territory, which is a concerning signal, as it has not yet managed to exit this zone.

The decline in precious metal prices is attributed to several factors, most notably the rebound in the US dollar index following the appointment of Kevin Warsh, who is known for his more hawkish stance on monetary policy, as well as his view that the Federal Reserve’s balance sheet should be tightened or reduced when necessary, under what is known as quantitative tightening (QT). In addition, investors were forced to liquidate positions to cover losses in other assets, particularly US technology stocks, due to margin calls. Changes to leverage rules at the Chicago exchanges also contributed to increased selling pressure on metals, alongside growing fears among retail investors and speculators, prompting some to exit their positions.

This raises the key question: have the fundamental factors supporting gold and silver come to an end, and should we expect further downside?

The answer is no, especially as there are two core and persistent factors that continue to support gold prices in the coming period, despite the elevated volatility. The first is the ongoing purchases by global central banks, which do not target specific price levels and therefore tend to look past short-term price fluctuations. The second is the decline in investor confidence in public finances and the widening fiscal deficits, particularly in advanced economies. This has led investors to reduce exposure to long-term government bonds, such as US, UK, French, German, and Japanese bonds, which are facing selling pressure and rising yields, pushing investors toward gold as a traditional safe haven.

In addition, ongoing trade and geopolitical tensions and inflationary risks continue to support gold. US inflation remains above the 2% target, with the core Producer Price Index registering 3.3%, alongside uncertainty surrounding the independence of the Federal Reserve following the end of Jerome Powell’s term.

As for silver, the persistent supply deficit combined with strong industrial demand continues to provide supportive fundamentals for prices in the medium term.

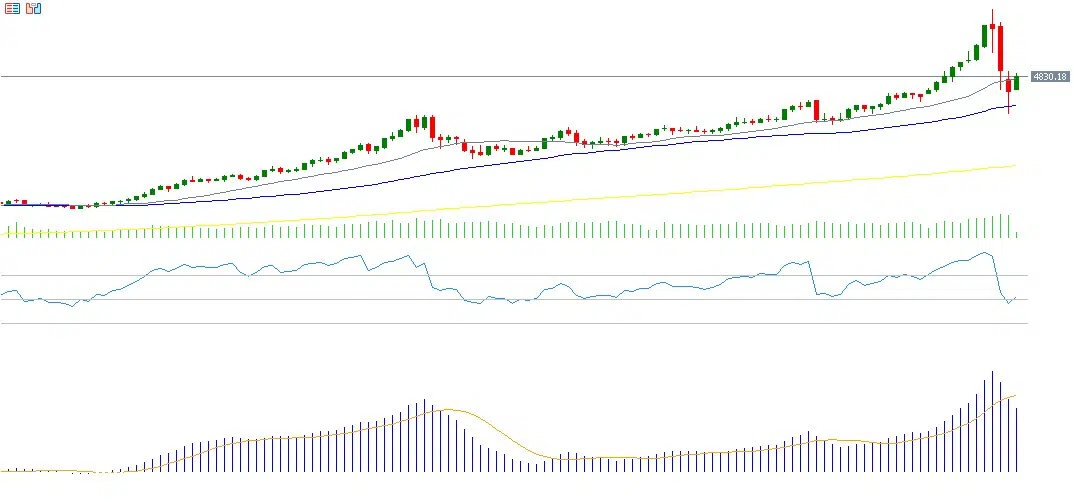

From a technical perspective, gold prices are currently trading below the 20-day moving average but remain above the 50-day moving average. A break below this level could open the door for a decline toward the 100-day moving average near USD 4,200. Regarding technical indicators, the Relative Strength Index is currently at 53, reflecting positive momentum, while the MACD is trading below the signal line, indicating continued bearish momentum for the asset.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.