Key Events of Last Week

United States of America

- The Federal Reserve decided to cut interest rates by 50 basis points from the range of 5.25% – 5.50% to 4.75% – 5.00%, marking the first reduction since March 2020.

- The Philadelphia Fed Manufacturing Index declined, registering a growth of 1.7 points, which is below expectations (-0.8) and the previous reading (-7.0).

- The unemployment claims index fell to 219,000, a figure lower than expectations (230,000) and the previous reading (231,000).

- S. oil inventories decreased by 1.630 million barrels, a number lower than expectations (-0.200 million) and the previous reading (0.833 million).

- The building permits index rose to 1.475 million, which is higher than expectations (1.410 million) and the previous reading (1.406 million).

- The Empire State Manufacturing Index in New York increased to 11.50 points, higher than expectations (-4.10) and the previous reading (-4.70).

- The retail sales index grew by 0.1% month-on-month, higher than expectations (-0.2%) but lower than the previous reading (1.1%).

- The industrial production index grew by 0.8% month-on-month, which is higher than expectations (0.2%) and the previous reading (-0.9%).

- The existing home sales index declined to 3.86 million, a figure lower than expectations (3.92 million) and the previous reading (3.96 million).

Eurozone

- The headline Consumer Price Index (CPI) grew by 2.2% year-on-year, matching expectations but lower than the previous reading (2.6%). The core CPI (excluding food and energy) also grew by 2.8% year-on-year, matching expectations but lower than the previous reading (2.9%).

United Kingdom

- The Bank of England decided to keep interest rates steady at 5.00%, in line with expectations.

- The headline CPI grew by 2.2% year-on-year, matching both expectations and the previous reading. The core CPI (excluding food and energy) grew by 3.6% year-on-year, matching expectations but lower than the previous reading (3.3%).

- The retail sales index rose by 2.3% year-on-year, a figure higher than expectations (1.1%) and the previous reading (1.4%).

Canada

- The Consumer Price Index decreased year-on-year, registering a growth of 2.0%, which is lower than the previous reading (2.5%).

Australia

- The change in employment rate recorded 47.5 thousand new jobs, which is higher than expectations (26.4 thousand) but lower than the previous reading (48.9 thousand).

- The unemployment rate stood at 4.2%, in line with expectations and the previous reading.

Japan

- The Bank of Japan decided to keep interest rates steady at 0.25%, in line with expectations.

- The exports index declined year-on-year, registering a growth of 5.6%, which is lower than expectations (10.0%) and the previous reading (10.2%).

- The imports index also declined year-on-year, registering a growth of 2.3%, which is lower than expectations (13.4%) and the previous reading (16.6%).

- The headline CPI grew by 3.0% year-on-year, which is higher than the previous reading (2.8%). The core CPI (excluding food) also grew by 2.8% year-on-year, matching expectations but higher than the previous reading (2.7%).

China

- The People’s Bank of China maintained the five-year loan prime rate at 3.85%, in line with expectations. It also kept the one-year loan prime rate at 3.35%, matching expectations.

Key Events This Week

Markets are awaiting several important economic indicators and data this week:

- Today, the Purchasing Managers’ Index (PMI) for both the industrial and service sectors will be released in Australia, the Eurozone, the UK, and the United States.

- On Tuesday, markets will be looking forward to the interest rate decision from the Reserve Bank of Australia, with expectations to keep rates steady at 4.35%. Additionally, the PMIs for the industrial and service sectors in Japan, as well as the Consumer Confidence Index in the U.S., will be released.

- On Wednesday, markets will be watching for building permits, new home sales, and U.S. crude oil inventories.

- On Thursday, the Swiss National Bank’s interest rate decision is anticipated, with expectations of a 25 basis point cut from 1.25% to 1.00%. Also, durable goods orders, GDP, unemployment claims, and pending home sales will be released in the U.S. Furthermore, markets are awaiting remarks from the Chair of the U.S. Federal Reserve, Jerome Powell.

- Finally, on Friday, markets will look for the Consumer Price Index in Tokyo, the Consumer Confidence Index in the Eurozone, and the core Personal Consumption Expenditures Price Index and Michigan Consumer Sentiment Index in the U.S., along with Canada’s GDP.

Technical Analysis

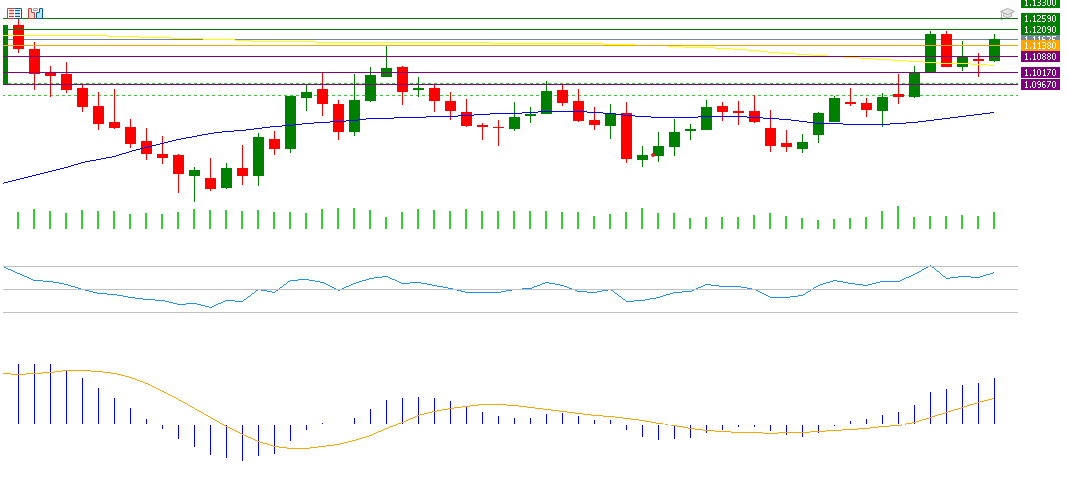

EUR/USD

If the pivot point of 1.1138 for the euro against the dollar is broken, there is a possibility of targeting support levels at 1.1088, 1.1017, and 1.0967. If it exceeds the pivot point, it may target resistance levels at 1.1209, 1.1259, and 1.1330.

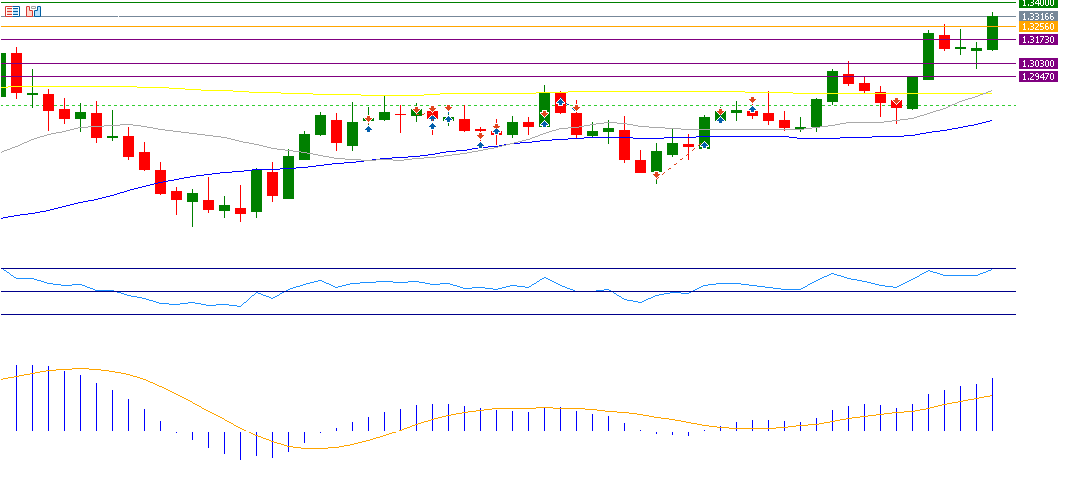

GBP/USD

If the pivot point of 1.3256 for the pound against the dollar is broken, there is a possibility of targeting support levels at 1.3173, 1.3030, and 1.2947. If it exceeds the pivot point, it may target resistance levels at 1.3400, 1.3482, and 1.3625.

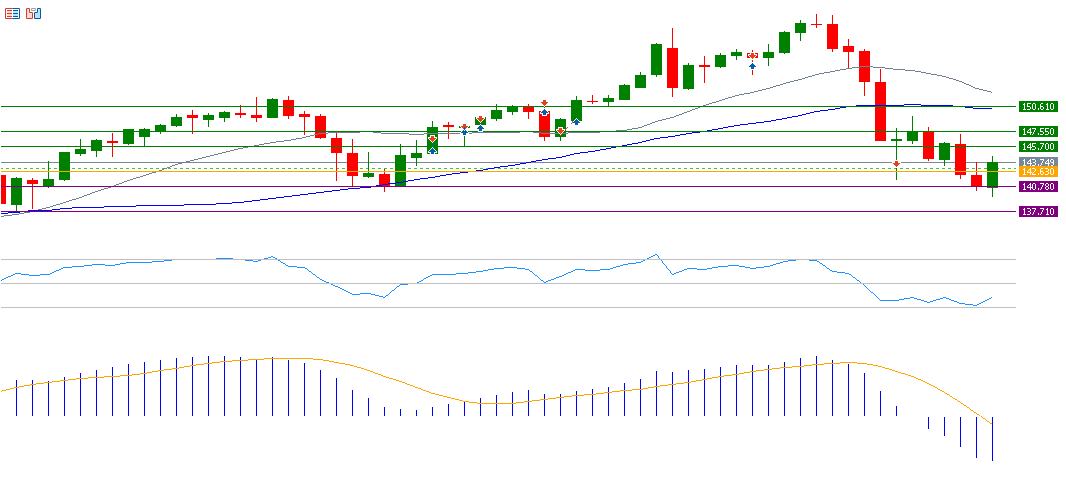

USD/JPY

If the pivot point of 142.63 for the yen against the dollar is broken, there is a possibility of targeting support levels at 140.78, 137.71, and 135.86. If it exceeds the pivot point, it may target resistance levels at 145.70, 147.55, and 150.61.

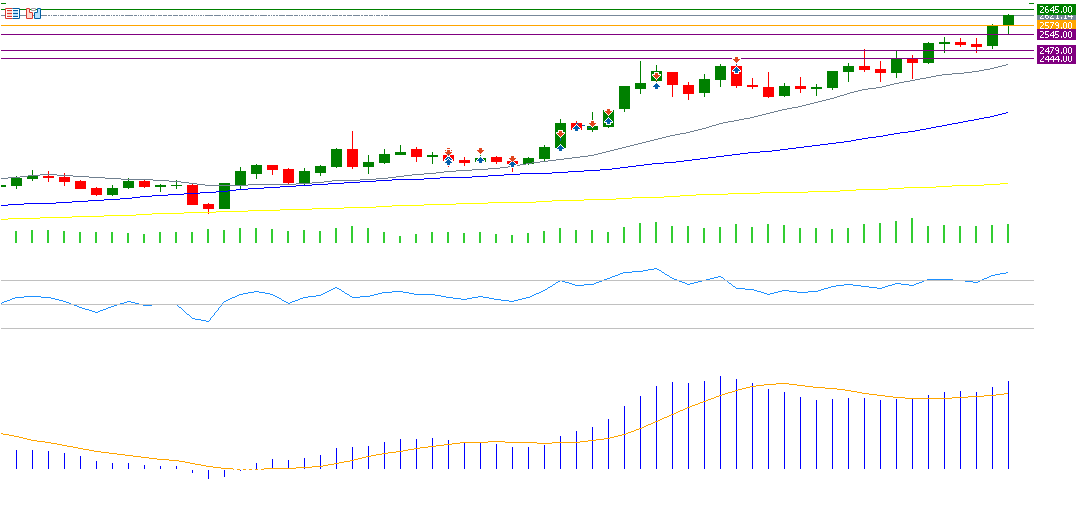

Gold (XAU)

If the pivot point of 2579 for gold is broken, there is a possibility of targeting support levels at 2545, 2479, and 2444. If it exceeds the pivot point, it may target resistance levels at 2645, 2680, and 2745.

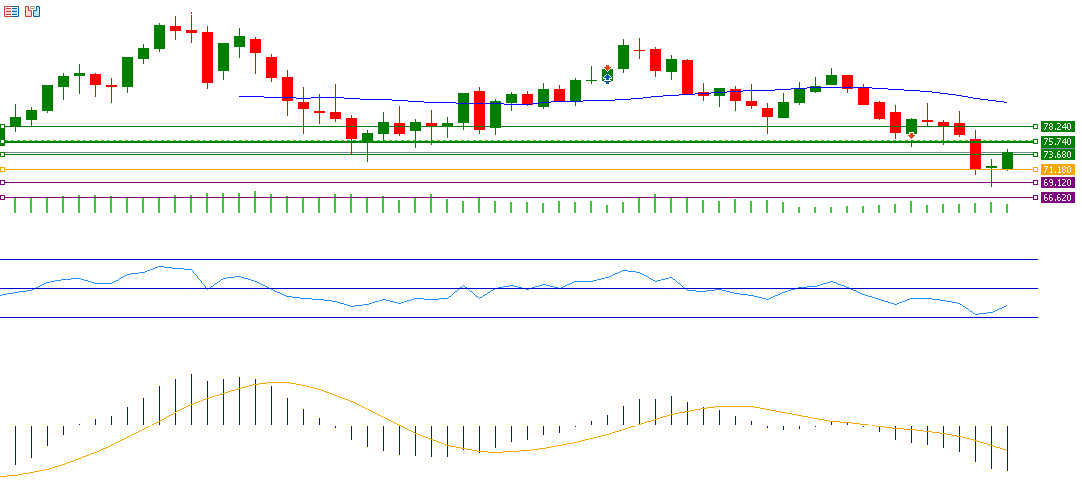

Brent Crude Oil

If the pivot point of 71.18 for crude oil is broken, there is a possibility of targeting support levels at 69.12, 66.62, and 64.56. If it exceeds the pivot point, it may target resistance levels at 73.68, 75.74, and 78.24.

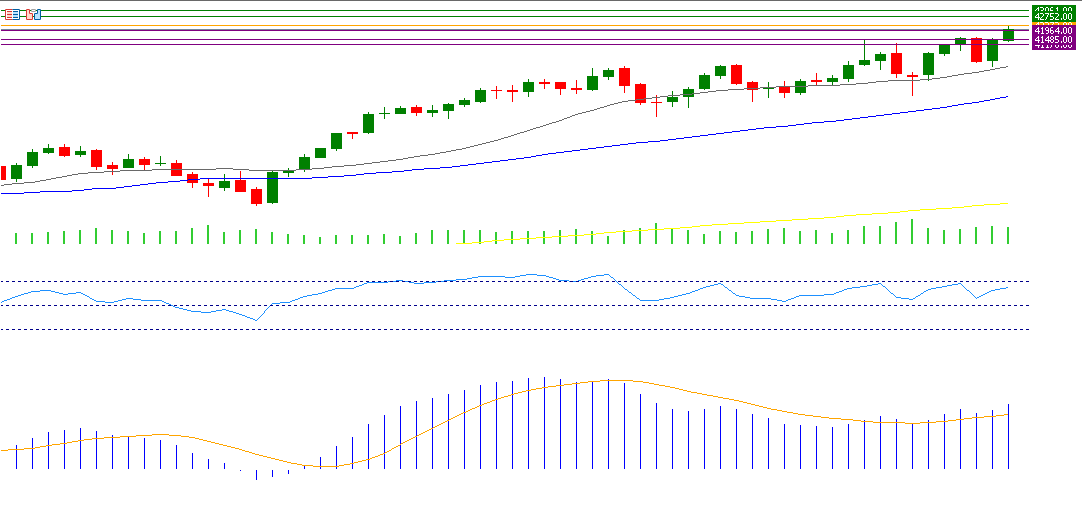

US30

If the pivot point of 42273 for the Dow is broken, there is a possibility of targeting support levels at 41964, 41485, and 41176. If it exceeds the pivot point, it may target resistance levels at 42752, 43061, and 43540.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.