Precious metals markets are experiencing high volatility in the current environment amid ongoing conflict. Gold prices have declined significantly by 27% from their peak on January 29, 2026, at $5,600 to a recent low of around $4,100, and are currently trading below $4,400, still up about 1% since the beginning of the year.

There are three main factors weighing on gold:

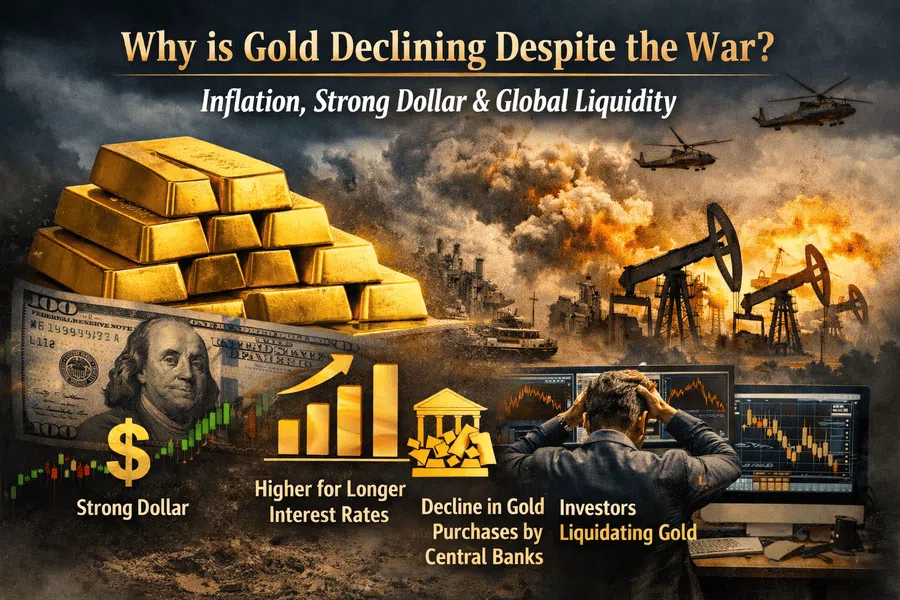

First, the strength of the US dollar amid inflation concerns. Recent inflation readings, such as Core PCE and Core PPI for February—before the outbreak of the war—came in higher, which is concerning, especially as the conflict may further fuel inflation due to rising energy prices. This comes alongside the hawkish tone of Jerome Powell, who emphasized that there will be no rate cuts until inflation declines and that interest rates must remain restrictive to bring inflation back to target. He also noted that some Federal Reserve members have discussed the possibility of rate hikes. As a result, keeping interest rates higher for longer, or even raising them further, puts pressure on gold as a non-yielding asset.

Second, the decline in gold purchases by central banks, which are prioritizing maintaining higher US dollar liquidity. This is particularly important given rising oil and gas prices, which require greater dollar allocations for energy imports. As a result, central banks are balancing between holding higher dollar reserves and continuing gold purchases and have opted to reduce gold buying in this phase.

Third, gold liquidation by both individual and institutional investors, as it has been one of the most profitable assets. Investors are selling gold to cover losses in other markets, particularly equities.

Looking ahead, expectations suggest that gold could resume its upward trend once the conflict subsides, especially as several supportive factors remain in place. These include its role as an inflation hedge and a shift away from long-term government bonds—such as US, UK, French, German, and Japanese bonds—which are facing selling pressure and rising yields due to declining confidence in fiscal conditions and widening deficits. This has historically driven investors back toward gold as a traditional safe haven, alongside the potential return of central bank buying.

As for industrial metals such as silver, palladium, and platinum, they remain at risk in the current environment. A slowdown in global industrial activity due to higher energy prices could lead to weaker demand for these metals.

From a technical perspective, gold is showing signs of weakness. The 20-day moving average at $4,990 is converging with the 50-day moving average at $4,969, with a bearish crossover emerging, which may indicate a shift toward a downward trend. The 200-day moving average at $4,096 is considered a key support level; prices approached it but failed to break below, suggesting strong support. The Relative Strength Index stands at 27, indicating negative momentum, while a bearish crossover between the MACD line and the signal line further supports the likelihood of continued downside pressure.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.