July 1, 2026

By Connor Woods, Global Head of Trading Education | 1 July 2026

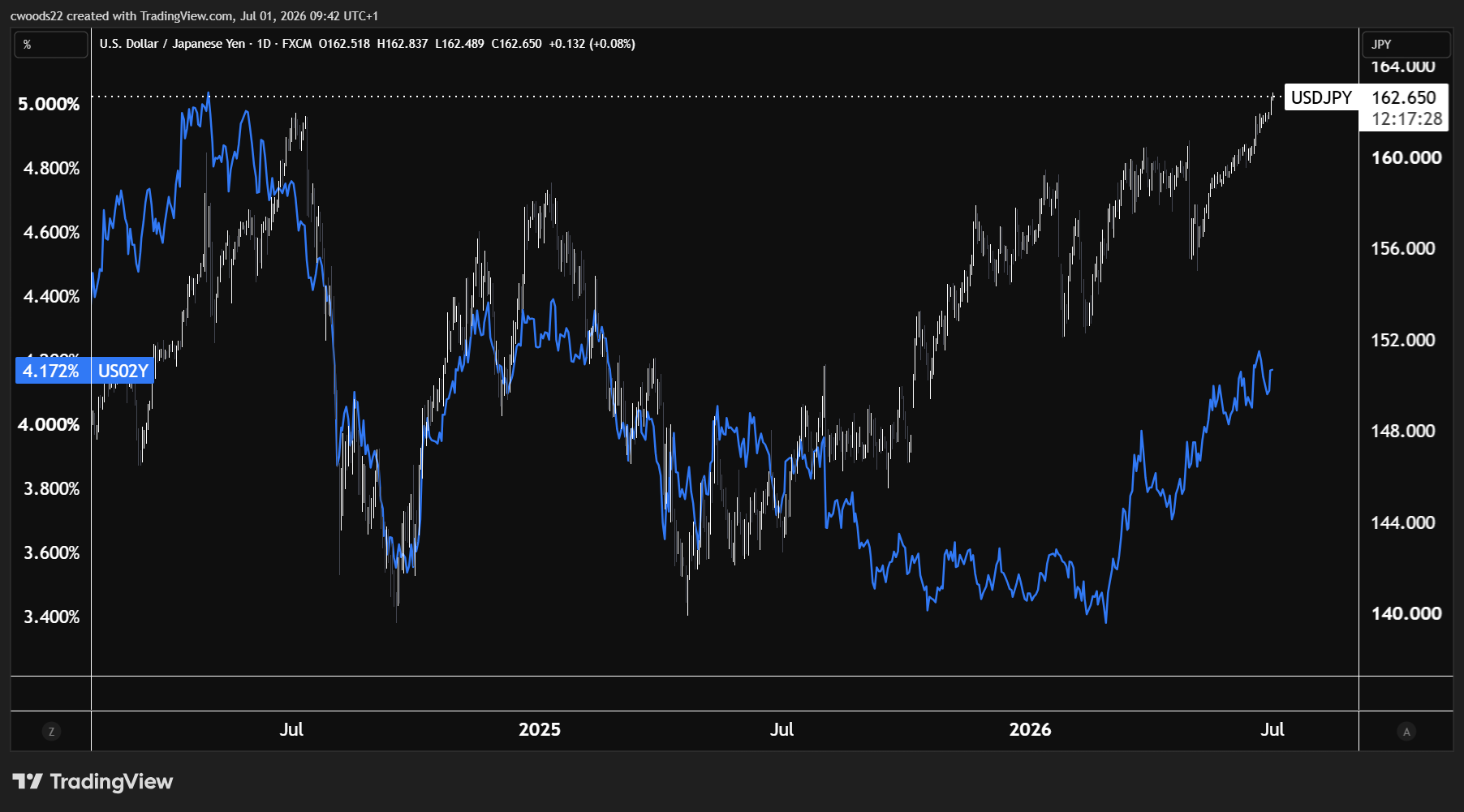

For two years, USD/JPY and the US 2 year yield have told the same story. When yields rose, the yen weakened. When yields fell, the yen strengthened. It was one of the cleanest correlations in macro. But that relationship has started to crack, and the daily chart reveals exactly where and why.

Key Points

- USD/JPY at 162.65 has hit its weakest level since 1986, but here is the problem: when the US 2 year yield was at the same 4.17% level in late 2024, USD/JPY was trading around 148 to 150. The same yield now corresponds to a rate 12 to 14 big figures higher. The correlation that held for two years has broken, and USD/JPY is running far ahead of what the rate differential justifies.

- The positioning data is at extremes not seen since the July 2024 carry trade unwind. CFTC net short yen sits at $11.3 billion, leveraged money is at the 3rd percentile of its 52 week range (net short 97,092 contracts), and asset managers are also net short 78,364 contracts. When both sides of the institutional market are aligned at an extreme, the snapback risk is significant. Retail sentiment at 86% short USD/JPY adds fuel to the contrarian case.

- The Bank of Japan hiked to 1.00% on June 16 (from 0.75%) and spent ¥11.7 trillion ($73.5 billion) on intervention in May, yet the yen is still making new multi decade lows. The rate differential has actually narrowed from 475 basis points in mid 2024 to 250 to 275 basis points today. By that measure, USD/JPY should be lower, not higher. Something beyond rates is driving this pair, and VIP clients need to understand what it is before the next unwind begins.

The Chart That Tells the Story

Chart: USD/JPY (candlesticks) vs US 2-Year Yield (blue line), Daily timeframe (TradingView)

Two Years of Moving Together

The logic behind this correlation is straightforward. The US 2 year yield reflects where the market expects Fed policy rates to be over the next 24 months. When that yield rises, it means traders expect rates to stay higher for longer, which makes holding US dollars more attractive relative to the yen. Money flows from Japan (where rates are low) into the US (where rates are high) to capture that yield difference. This is the carry trade in its simplest form, and it has been the dominant force behind USD/JPY for the past two years.

The daily chart shows this playing out in four clean phases. From April to July 2024, both USD/JPY and the 2 year yield peaked together, with the pair touching 164 and the yield pushing toward 5.0%. Then came the summer 2024 carry trade unwind: the yield crashed from 5.0% to 3.5% as the Fed began cutting rates, and USD/JPY fell from 164 to 140 in near perfect lockstep. Through 2025, both assets chopped in a range, with USD/JPY between 140 and 156 and the 2 year yield between 3.5% and 4.3%, still moving together. By late 2025, both had bottomed, with USD/JPY around 139 to 140 and the yield near 3.4%.

The correlation coefficient through these four phases stayed consistently above 0.80. It was one of the most reliable macro relationships in the market. Knowing where the 2 year yield was heading gave you a strong read on where USD/JPY was going. That reliability is what makes the current divergence so important.

Same Yield, Different Price

Here is the number that should make every VIP client sit up. The US 2 year yield today is 4.172%. In late 2024, when the yield was at the same 4.17% level, USD/JPY was trading around 148 to 150. Today, with the yield at the exact same level, USD/JPY is at 162.65. That is 12 to 14 big figures higher for the same yield. The correlation that held so tightly for two years has broken in a specific direction: USD/JPY is overshooting what the rate market says it should be.

What makes this even more striking is the rate differential. In late 2024, the BoJ policy rate was around 0.25%, giving a differential of roughly 390 basis points in the dollar’s favour (4.17% minus 0.25%). Today, the BoJ has hiked to 1.00% after raising rates on June 16, so the differential is now roughly 317 basis points (4.17% minus 1.00%). The gap between US and Japanese rates has actually narrowed by 73 basis points, yet USD/JPY is 12 to 14 big figures higher. By the logic that drove this pair for two years, it should be lower, not at multi decade highs.

So what is driving the overshoot? Three forces are at work beyond the simple rate differential. First, carry trade momentum. When a trade works for months on end, capital piles in and price moves beyond what fundamentals justify. The carry trade on USD/JPY is generating roughly 2.5% annualised return just from the yield pickup, which attracts more capital, which pushes USD/JPY higher, which generates even more return in yen terms. It is a self reinforcing loop until it breaks. Second, Japan’s structural trade deficit. Energy imports remain elevated and the weaker yen inflates the cost of those imports, widening the deficit and creating natural selling pressure on the yen. Third, intervention fatigue. The Bank of Japan spent ¥11.7 trillion ($73.5 billion) on yen buying operations in May and it did not hold. The market has called the BoJ’s bluff, and every failed intervention emboldens the short yen trade.

The Positioning Extreme

This is where it gets critical. The latest Commitment of Traders data shows leveraged money net short 97,092 JPY contracts, sitting at the 3rd percentile of the trailing 52 week range with a z score of negative 1.46. The 52 week range runs from negative 99,844 to positive 38,497, which means current positioning is within 3,000 contracts of the most extreme short yen reading of the entire past year. Asset managers are also net short 78,364 contracts, making this an aligned positioning signal where both institutional categories agree. That alignment amplifies the risk because there is no natural buyer of size when everyone is on the same side.

The CFTC aggregate net short yen position stands at $11.3 billion, which is comparable to the level reached in July 2024, just before the carry trade unwind sent USD/JPY from 162 to 140 in the space of three weeks. That unwind was triggered by a combination of a BoJ rate hike and weaker than expected US payrolls data that shifted rate expectations. Today, we have a remarkably similar setup: the BoJ just hiked on June 16, and NFP drops tomorrow with a forecast of 114,000, down significantly from 172,000. History may not repeat, but the parallels are hard to ignore.

On the retail side, Myfxbook data shows 86% of traders are short USD/JPY, betting on yen strength. Only 14% are long. That is one of the most extreme retail readings on any major pair. From a contrarian perspective, when 86% of retail is positioned one way, price tends to move the other direction, which in this case means higher USD/JPY. But here is the nuance: at some point, the crowd is right about the direction, just wrong about the timing. The question is whether the structural forces (narrowing rate differential, BoJ hiking cycle, intervention risk) overwhelm the momentum forces (carry returns, self reinforcing flows, intervention fatigue) in the weeks ahead.

What Snaps It Back

The divergence between USD/JPY and the 2 year yield will resolve in one of two ways. Either the yield needs to rise sharply toward 4.5% to 4.8% to justify where USD/JPY is trading, or USD/JPY needs to fall back toward 150 to 155 to realign with the current yield. Given that Warsh’s Fed has pushed the dot plot to 3.8% year end and Core PCE just printed at 3.4% annually (the highest since October 2023), yields could certainly rise further. But the market is already pricing aggressive rate expectations, and the 2 year would need to make a significant move to justify 162.

The more likely resolution is a snapback in USD/JPY toward the level that the 2 year yield actually justifies. The catalyst could come from several directions. Tomorrow’s NFP (forecast 114,000) is the most immediate risk. A miss below 100,000 would drop the 2 year yield sharply as rate hike expectations get repriced, and with positioning this extreme, the unwind in USD/JPY would be violent. Today’s Sintra panel with Warsh, Lagarde, Bailey, and Macklem is another wildcard. If Warsh shows any softening in tone during his first international appearance, it would pull the 2 year yield lower and USD/JPY with it.

BoJ board member Tamura has outlined a path of hiking 25 basis points every few months toward a neutral rate of 2%. If the BoJ follows through on that path, the differential narrows further, removing the fundamental anchor of the carry trade. Japanese institutional investors have already begun repatriating capital, with foreign selling of US Treasuries from Japanese accounts spiking earlier this year as domestic yields become attractive enough to bring money home. That repatriation flow is structural and works against USD/JPY over the medium term.

The levels to watch: on the upside, 164 is the June 2024 high and the area where the BoJ last intervened at scale. A move above 164 would almost certainly trigger another round of intervention. On the downside, 158 is the first meaningful support from the May consolidation, and 155 is where the 2 year yield correlation suggests fair value sits. If the snapback begins, the speed of the unwind should not be underestimated. The July 2024 move from 162 to 140 took just 20 trading days. With positioning at identical extremes, a repeat of that magnitude is not out of the question.

Risk Warning: Trading financial instruments, particularly those involving leverage, involves a substantial degree of risk and is not appropriate for all investors. The value of your investments can rise or fall sharply, and it is possible to lose the entirety of your invested capital. Do not trade with funds you cannot afford to lose. Nothing in this site should be read or construed as constituting advice on the part of Taurex or any of its affiliates, directors, officers or employees.