Last week saw the release of a mixed set of economic data across major economies. The United States reported several indicators reflecting a relative slowdown in some areas alongside persistent inflationary pressures. The ISM Non-Manufacturing PMI declined to 54.0 points, below both expectations and the previous reading, while U.S. crude oil inventories increased by 3.081 million barrels during the past week. On the inflation front, the headline Consumer Price Index recorded annual growth of 3.3%, while core inflation reached 2.6%. The Core Personal Consumption Expenditures Price Index also registered growth of 3.0%. Meanwhile, durable goods orders declined by 1.4% on a monthly basis, despite core durable goods orders excluding transportation rising by 0.8%. Economic growth also slowed, with fourth-quarter GDP expanding by only 0.5%, while initial jobless claims increased to 219,000. In addition, the University of Michigan Consumer Sentiment Index declined to 47.6 points, reflecting increased caution among consumers regarding the economic outlook. In Europe, the Eurozone services PMI recorded a slight expansion above expectations but slowed compared to the previous reading, while services activity in the United Kingdom weakened and the construction sector remained in contraction despite a modest improvement. In Canada, the Ivey PMI unexpectedly contracted despite stronger employment and a slight decline in the unemployment rate. In Australia, services activity returned to contraction territory, while the Reserve Bank of New Zealand kept interest rates unchanged at 2.25% as expected. In Asia, Japanese data showed improvement in wages and corporate goods prices with modest growth in household spending, while China recorded slower consumer inflation alongside a noticeable improvement in producer prices, which reached their highest level since September 2022.

Market Analysis

USD/JPY

The USD/JPY pair reached a level of 160.46 on Monday, March 30, 2026, its highest level since July 11, 2024. The pair closed on Friday at 159.24, up about 1.50% since the beginning of the year. Expectations indicate that the pair may continue its positive momentum with the potential to reach the 162.00 level, which was last recorded on July 3, 2024. It is worth noting that whenever USD/JPY reaches levels of 160 and above, Japanese officials tend to intervene either verbally or directly by selling U.S. dollars and buying Japanese yen in order to support the local currency. Expectations also suggest that the Bank of Japan may continue monetary tightening, potentially raising interest rates at its next meeting, amid divergence between monetary and fiscal policies. The fiscal policy adopted by Japanese Prime Minister Sanae Takaichi is expansionary, involving increased spending and tax cuts to support the economy, which creates uncertainty within Japan amid discussions about the possibility of the economy entering a stagflationary phase. The Relative Strength Index (RSI) currently stands at around 54 points, indicating positive momentum for the USD/JPY pair.

JP Morgan Chase

Shares of JP Morgan Chase have declined by about 4% since the beginning of the year. Markets are awaiting the bank’s first-quarter earnings results, scheduled for Tuesday, April 14, 2026. Analysts expect earnings per share to reach $5.38, compared with $5.07 in the previous reading. Revenue is expected to reach $48.62 billion after recording $46.00 billion previously. The Relative Strength Index (RSI) currently stands at 65 points, indicating positive momentum for JP Morgan Chase shares. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (blue) and the signal line (orange), suggesting positive momentum for the stock.

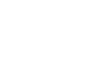

Silver

Silver prices have risen for the third consecutive week, closing at $75.93 on Friday and gaining about 6% since the beginning of the year. Over the past week, silver has been trading in a horizontal range between approximately $70 and $77, searching for a clear direction either upward or downward. The Relative Strength Index (RSI) currently stands at 50 points, indicating neutral momentum. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (blue) and the signal line (orange), suggesting positive momentum for silver.

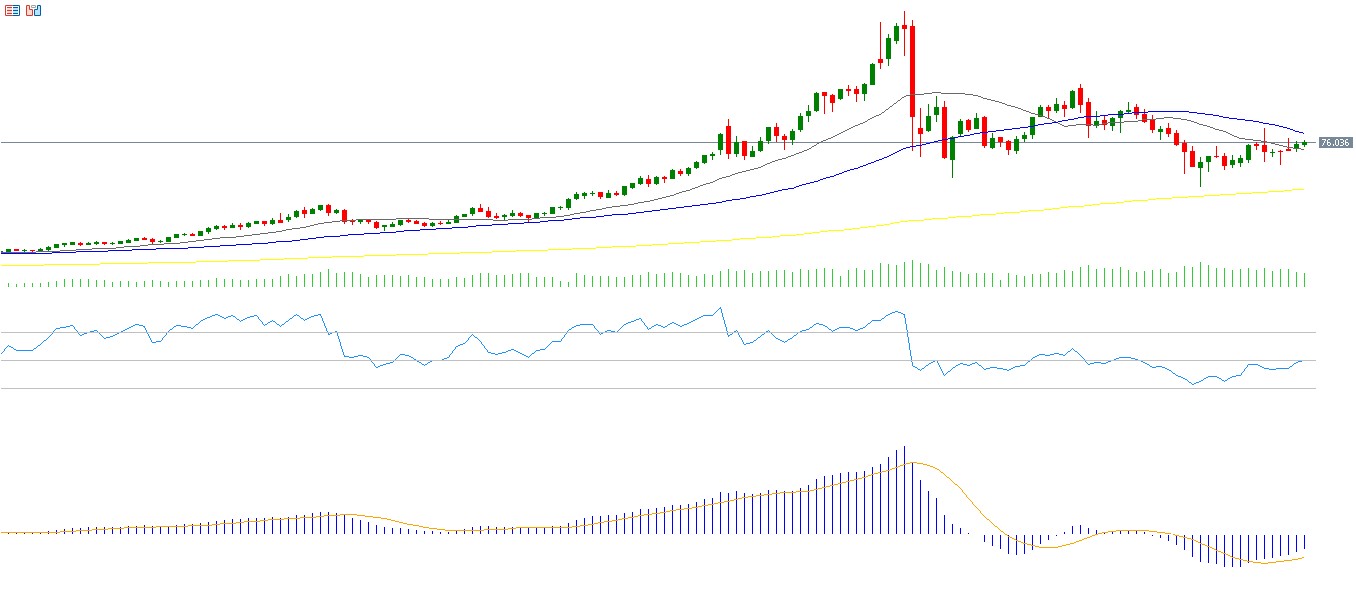

Nasdaq 100 Index

The Nasdaq 100 Index rose by 4.45% last week, closing at 25,116 points, its highest level since February 26, 2026. Despite this rise, the index remains down about 0.50% since the beginning of the year. The VIX volatility index declined to 19 points on Friday, its lowest level since February 27, 2026, reflecting investor optimism and increased demand for U.S. equities. However, despite this strong optimism, U.S. equity markets continue to face several risks during the current period, particularly uncertainty related to geopolitical tensions, inflation concerns, and fiscal risks. Notably, the Philadelphia Semiconductor Index reached a new record high on Friday, rising about 26% since the beginning of the year, reflecting strong optimism surrounding investments in semiconductors and artificial intelligence. The Relative Strength Index (RSI) currently stands at 60 points, indicating bullish momentum for the Nasdaq 100. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (blue) and the signal line (orange), providing upward momentum for the index.

Key Events This Week

Markets are closely monitoring several important economic indicators this week.

On Monday, markets will watch China’s new loans data and existing home sales in the United States.

On Tuesday, attention will turn to the British Retail Consortium retail sales report, industrial production in Japan, and the Producer Price Index in the United States.

On Wednesday, the Eurozone industrial production index and the Empire State Manufacturing Index in New York will be released, along with U.S. crude oil inventory data.

On Thursday, markets will focus on Australia’s unemployment rate and employment change figures, as well as China’s retail sales, industrial production, fixed asset investment, house price index, unemployment rate, and GDP data. The United Kingdom will release GDP and industrial production figures, Switzerland will publish its Producer Price Index, and the Eurozone will release its Consumer Price Index. In the United States, markets will also watch the Philadelphia Fed Manufacturing Index, industrial production data, and initial jobless claims.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.