Key Points

- Friday’s Non-Farm Payrolls report is the main event this week, with consensus expecting 60,000 jobs added and the unemployment rate holding at 4.3%. The previous reading came in at 178,000, so a significant drop would raise concerns about the health of the labour market.

- Last week’s FOMC decision saw the widest dissent since October 1992, with the committee splitting 8 to 4. The Fed held rates at 3.50% to 3.75%, but one member voted for a cut while three others pushed back against the easing bias in the statement. Powell confirmed he will step down as Chair on May 15.

- The Reserve Bank of Australia is expected to hike rates by 25 basis points on Tuesday, taking the cash rate from 4.10% to 4.35%. Gold has dropped to $4,576, falling for a second consecutive week as the hawkish Fed hold lifted the dollar and pushed Treasury yields higher.

The Macro Picture

Last week was enormous. Five central bank decisions, five mega cap tech earnings, and the first look at Q1 GDP all landed in the same week. The takeaway is that the economy is still growing (Q1 GDP came in at 2.0% annualised), corporate America is thriving (every major tech company beat expectations), and the Fed is in no rush to cut rates.

The headline from the FOMC was the dissent. The committee split 8 to 4, marking the widest disagreement since October 1992. One member, Stephen Miran, voted for a 25 basis point cut. Three others (Hammack, Kashkari, and Logan) wanted to remove the easing bias from the statement entirely. Jerome Powell confirmed during the press conference that he will step down as Chair on May 15, with Kevin Warsh’s Senate confirmation advancing the same day. The transition creates uncertainty around the direction of monetary policy, especially with inflation still running above target at 3.3%.

Big Tech delivered across the board. Apple reported revenue of $111.2 billion (up 17% year on year), Google Cloud revenue surged 63%, Meta revenue jumped 33%, and Microsoft beat earnings estimates by $0.21. The NASDAQ closed at a record 27,710 on Friday. This week, the focus shifts to Friday’s Non-Farm Payrolls and Tuesday’s RBA decision, with the ISM Services PMI and JOLTS Job Openings also due on Tuesday.

Gold: Bearish Structure but RSI Divergence Emerging

Chart: XAU/USD, H4 timeframe

Gold sits at $4,576, well below the all time high near $5,595 set earlier this year and down for a second consecutive week. The metal has been under sustained pressure since the FOMC held rates and delivered a hawkish tone, lifting the dollar and pushing Treasury yields higher. On the H4 chart, the structure is bearish with lower highs and bearish breaks of structure confirming the downtrend. The supply zone sits between $4,850 and $4,900, marked as a strong high, meaning sellers have been firmly in control at that level. On the downside, the key demand zone sits between $4,250 and $4,400, which is where buyers last stepped in aggressively.

The detail to watch is the RSI. While price has been making lower lows, the RSI has been making higher lows, which creates bullish divergence. This suggests that the selling pressure is starting to fade, even though the bearish structure remains intact. Divergence does not guarantee a reversal, but it is often an early warning that a bounce or shift in momentum could be developing.

The fundamental picture for gold is mixed. The hawkish Fed, strong dollar, and rising yields are all headwinds. The probability of a rate cut in June sits at just 5.1%, which removes one of the key bullish catalysts. On the other hand, the Strait of Hormuz remains closed, oil is above $100, and central banks continued to accumulate gold reserves in Q1. Friday’s Non-Farm Payrolls will be the key. A weak number would reignite rate cut hopes, weaken the dollar, and likely send gold bouncing toward the $4,850 to $4,900 supply zone. A strong number would reinforce the Fed’s hawkish stance and could push gold toward the $4,250 to $4,400 demand zone.

AUD/USD: RBA Rate Hike in Focus

Chart: AUD/USD, H4 timeframe

AUD/USD sits at 0.7196 heading into what could be a defining week for the Australian dollar. The Reserve Bank of Australia is expected to hike rates by 25 basis points on Tuesday, taking the cash rate from 4.10% to 4.35%. On the H4 chart, the structure is bullish with higher highs and higher lows, confirmed by multiple breaks of structure on the rally from the March lows around 0.6850. The most recent high near 0.7250 is labelled as a weak high, which suggests price could push through this level if the bullish momentum continues. The key demand zone sits between 0.7000 and 0.7050, which is where buyers stepped in during the most recent pullback.

The RSI is telling an important story. While price has been making higher highs, the RSI has been making lower highs, which creates bearish divergence. This is a warning that the rally may be running out of steam, even though the underlying structure remains bullish. A rate hike on Tuesday would typically support the Australian dollar, but if the move is already priced in, expect a “buy the rumour, sell the fact” reaction where AUD/USD pulls back after the announcement.

The combination of the RBA decision on Tuesday and the US Non-Farm Payrolls on Friday makes this a two catalyst week for AUD/USD. If the RBA hikes and Non-Farm Payrolls disappoint, AUD/USD could break through the 0.7250 weak high and push higher. If the RBA delivers a dovish hike (raising rates but signalling a pause) and Non-Farm Payrolls come in strong, the pair could pull back toward the 0.7000 to 0.7050 demand zone.

What to Watch This Week

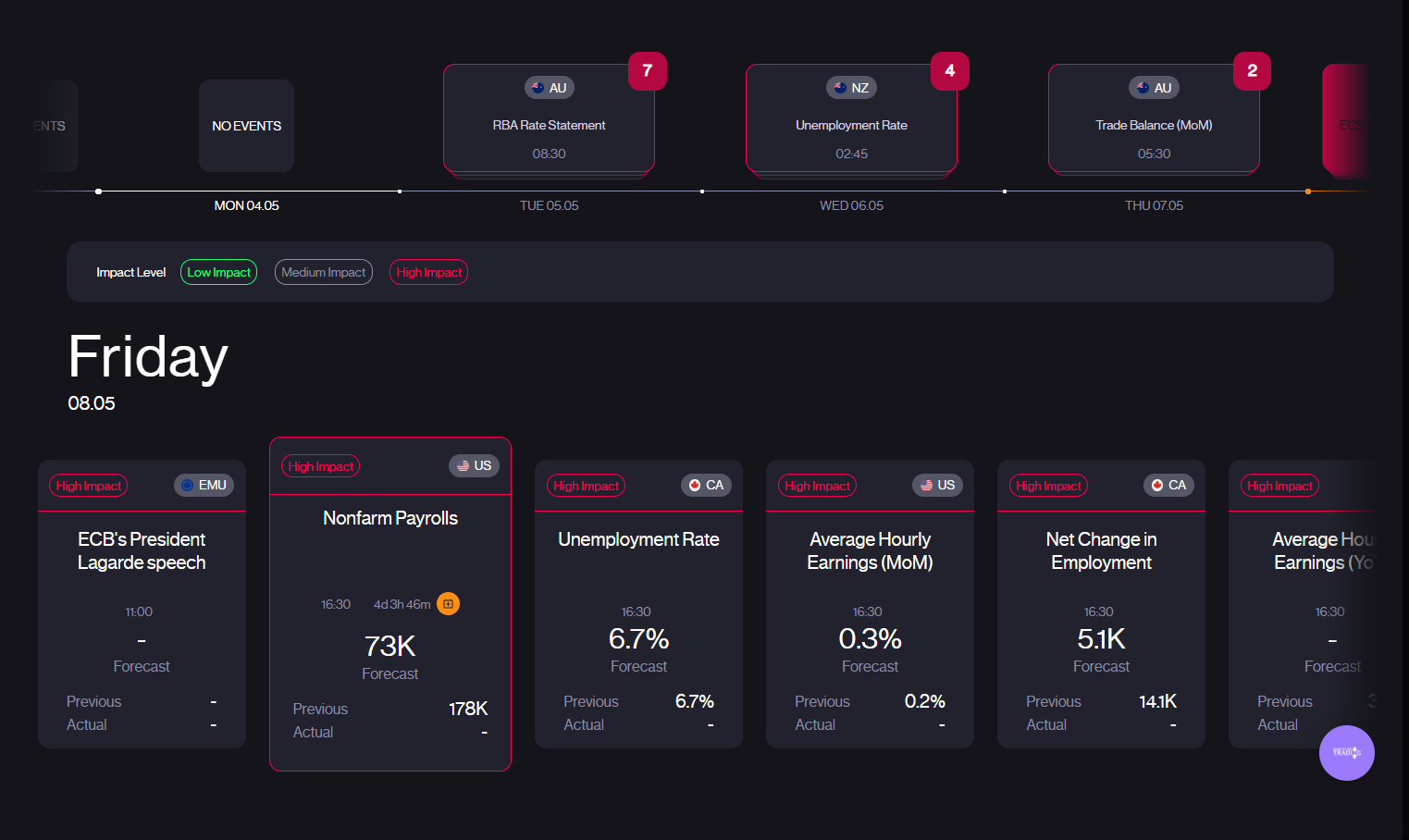

Tuesday is the busiest day on the calendar. The RBA rate decision lands first, with markets expecting a 25 basis point hike to 4.35%. The monetary policy statement and press conference will be closely watched for any signals about whether further hikes are on the table. Later on Tuesday, the ISM Services PMI arrives (forecast 53.8, previous 54.0), giving a read on how the largest part of the US economy is performing. JOLTS Job Openings also drops on Tuesday (forecast 6.87 million, previous 6.88 million), providing a look at labour demand.

Thursday is quiet, with no major releases scheduled. Friday is the main event. Non-Farm Payrolls (forecast 60,000, previous 178,000) and the unemployment rate (forecast 4.3%) will set the tone for the rest of May. Average hourly earnings (forecast 0.3%, previous 0.2%) will also be watched for signs of wage inflation. BoE Governor Bailey speaks on Friday, and Canadian employment data lands at the same time (forecast 5,100 jobs, unemployment 6.7%). Oil remains the wildcard throughout, with WTI around $101 after pulling back from $106 on ceasefire hopes late last week.

Editor note: Screenshot the Acuity calendar for May 4–8 2026. Key events: RBA Cash Rate + ISM Services PMI + JOLTS (Tue 5th), NZD Employment (Wed 6th), Non-Farm Payrolls + Unemployment Rate + Avg Hourly Earnings + BoE Gov Bailey Speaks + CAD Employment (Fri 8th).