Key Points

- Five central banks meet this week. The Federal Reserve announces on Wednesday in what could be Jerome Powell’s final meeting as Chair. The ECB follows on Thursday, with the Bank of Japan, Bank of Canada, and Bank of England also due. All five are expected to hold rates steady.

- The NASDAQ 100 is trading near fresh highs above 27,300, up 2.7% last week. Five of the seven largest tech companies report earnings this week, with Microsoft on Tuesday, Alphabet, Amazon, and Meta on Wednesday, and Apple on Thursday.

- Thursday is packed with the advance Q1 GDP reading, the PCE inflation gauge (the Fed’s preferred measure of price pressures), the ECB decision, and Apple earnings. Oil remains elevated with WTI around $96 and the Strait of Hormuz still closed.

The Macro Picture

This is one of the busiest weeks of the year. Five central bank decisions, five mega cap tech earnings, and two of the most important economic data releases on the calendar all land within the same five day window. The overarching question is whether the earnings momentum that has carried equities higher through April can continue, even as oil stays above $95 and the Strait of Hormuz remains closed.

Wednesday’s FOMC decision is the headline event. The Fed is widely expected to hold rates at 3.50% to 3.75% for the fourth consecutive meeting, but the real focus will be on the press conference. This could be Jerome Powell’s final appearance as Fed Chair, with his term ending on May 15 and the Senate committee voting on Trump’s nominee, Kevin Warsh, on April 29. Powell has spent eight years at the helm, and the transition to Warsh introduces a new set of uncertainties around monetary policy direction.

The ECB follows on Thursday, also expected to hold at 2.0%. The Eurozone economy is feeling the strain of the energy crisis, with the latest flash PMIs showing private sector activity contracting at the fastest pace since November 2024. Germany has halved its 2026 growth forecast, blaming the energy shock from the Middle East conflict. On the data side, Thursday delivers both the advance Q1 GDP estimate (the Atlanta Fed’s GDPNow model points to just 1.2% annualised growth) and March PCE data, with headline inflation running at 3.3% and the oil driven spike still working through the numbers.

NASDAQ 100: Earnings Season Takes Centre Stage

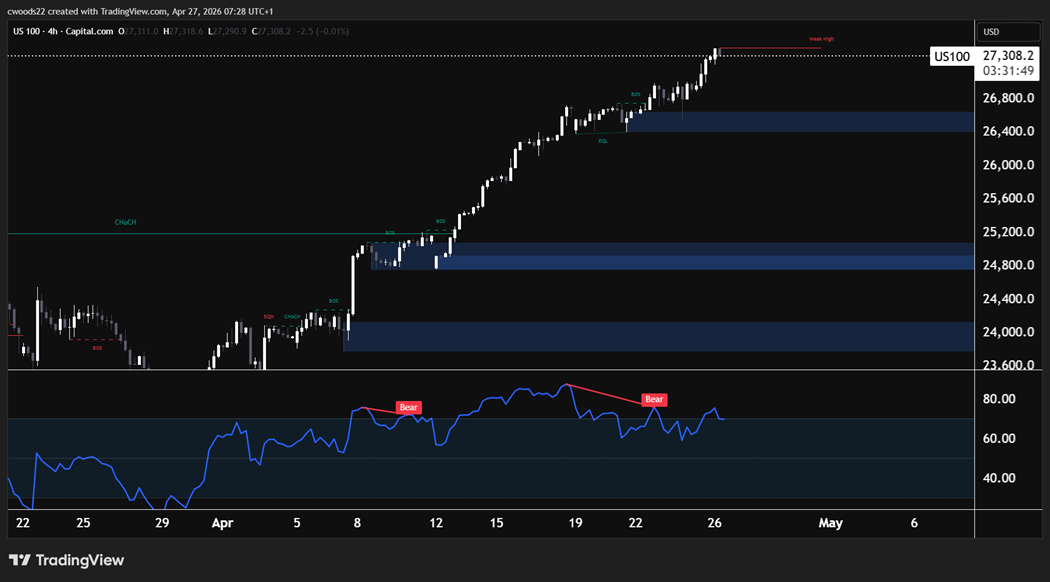

Chart: NASDAQ 100, H4 timeframe

The NASDAQ 100 sits at 27,308, trading near fresh highs after rallying 2.7% last week. The index has surged from around 23,600 in late March, gaining over 15% in less than a month. On the H4 chart, the structure is a clear uptrend with higher highs and higher lows, confirmed by multiple breaks of structure on the way up. The first key support zone sits around 25,000 to 25,200, which is where buyers stepped in during the most recent consolidation. Below that, the 24,000 area is the next major demand zone. There is no overhead resistance since price is at all time highs.

The standout detail on the chart is the RSI. While price has been making higher highs, the RSI has been making lower highs, which creates what is known as bearish divergence. This does not mean the trend is about to reverse, but it does signal that momentum is fading and a pullback would not be unusual, especially with five mega cap earnings landing this week.

Microsoft reports on Tuesday after the bell, with analysts watching Azure cloud revenue (expected at $34.2 billion, up 28% year on year). Alphabet, Amazon, and Meta all report on Wednesday, followed by Apple on Thursday. The key theme across all five is AI capital expenditure and whether the massive spending is translating into revenue growth. Each stock has rallied more than 10% this month except Apple at around 6%. If the results beat expectations, the NASDAQ could push toward 28,000 and beyond. If the numbers disappoint or forward guidance softens, watch for a pullback toward the 25,000 to 25,200 support zone.

EUR/USD: Central Banks in the Spotlight

Chart: EUR/USD, H4 timeframe

EUR/USD sits at 1.1719 after a sharp reversal from the April highs. The pair rallied from around 1.1650 to above 1.1850 in early April as the dollar sold off on Hormuz related uncertainty, but sellers have taken control since then. On the H4 chart, the structure has turned bearish with lower highs and lower lows from the 1.1850 area. There is a clear resistance zone around 1.1830 to 1.1850, which is where sellers have been stepping in consistently. On the downside, the key support zone sits around 1.1630 to 1.1650, which is where buyers came in during the early April rally. The RSI at 45 is showing bearish momentum, with divergence that supports the recent move lower.

This week’s price action will be driven almost entirely by central bank decisions. The Fed on Wednesday and the ECB on Thursday represent two of the three most important central banks in the world making policy decisions within 24 hours of each other. Both are expected to hold, which in isolation would be a neutral outcome for the pair. However, the tone of the press conferences will matter. If Powell signals that the Fed is in no rush to cut rates and emphasises inflation concerns from the oil shock, the dollar could strengthen and push EUR/USD back toward the 1.1650 support zone. If the ECB strikes a more hawkish tone and signals rate hikes are coming later in the year, the euro could rally back toward the 1.1850 resistance.

The Bank of Japan decision on Monday adds another layer. The BoJ is expected to hold at 0.75%, but any surprise hawkish shift could strengthen the yen and create broader dollar weakness, which would support EUR/USD. With three major central bank decisions in five days, expect elevated volatility across all currency pairs.

What to Watch This Week

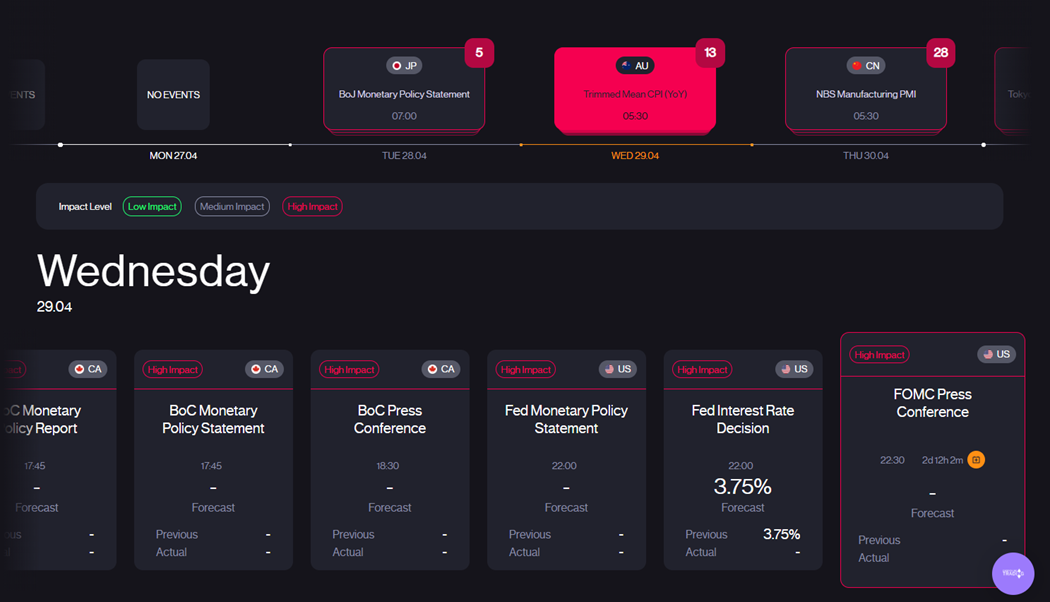

Monday kicks off with the Bank of Japan rate decision, expected to hold at 0.75%. Tuesday brings Microsoft earnings after the bell, which will set the tone for the rest of Big Tech. Wednesday is loaded with the FOMC decision at 6:00 PM GMT, Powell’s press conference, and earnings from Alphabet, Amazon, and Meta after the bell. Thursday may be even bigger, with the ECB rate decision, the Bank of England decision, the advance Q1 GDP reading, March PCE inflation data, and Apple earnings all on the same day. Friday rounds out with the ISM Manufacturing PMI.

The sheer volume of events means that Wednesday and Thursday alone could reshape the outlook for equities, currencies, and commodities heading into May. Oil remains the wildcard throughout, with WTI at $96 and Brent at $107 as the Strait of Hormuz stays closed and peace talks remain stalled. Any headline from the Middle East could override everything on the economic calendar.

Editor note: Screenshot the Acuity calendar for April 27 – May 1 2026. Key events: BoJ decision (Mon 27th), Microsoft earnings (Tue 28th after bell), FOMC decision + Powell press conf + GOOG/AMZN/META earnings (Wed 29th), ECB decision + BoE decision + Q1 GDP advance + PCE + Apple earnings (Thu 30th), ISM Manufacturing PMI (Fri 1st).