Last week witnessed the release of several important economic data points that reflected a mixed picture of the global economy. In the United States, data showed that inflation remained relatively stable near expectations, while GDP growth slowed and durable goods orders weakened. This came alongside some resilience in the labor market and stronger existing home sales. In the Eurozone, industrial production declined significantly on a monthly basis, reflecting ongoing pressure on the manufacturing sector. In the United Kingdom, the economy showed clear signs of slowing, with GDP posting zero monthly growth and industrial production declining. In Canada, signs of weakness appeared in the labor market as unemployment increased and a large number of jobs were lost. Meanwhile, consumer confidence improved in Australia compared with the previous reading. In Japan, household spending declined significantly despite a slight improvement in GDP growth in the fourth quarter. In China, economic data showed notable improvement, with inflation, exports, and imports rising strongly above expectations, indicating a partial recovery in both domestic and external demand.

Market Analysis

USD / Danish Krone

The US dollar against the Danish krone reached 6.5485 on Friday, its highest level since August 1, 2025. The pair has risen by about 3% since the beginning of the year. Recent Danish economic data indicate weakness in economic performance, as both consumer price index figures and GDP for the fourth quarter of last year declined.

It is worth noting that one of the key factors supporting the USD/DKK pair recently has been the strength of the US dollar, with the US Dollar Index reaching its highest level since May 29, 2025. The dollar is considered a safe-haven asset amid rising geopolitical tensions, particularly the ongoing conflict involving the United States and Israel against Iran, alongside growing concerns about a potential expansion of the conflict amid uncertainty regarding its duration and outcome. In addition, expectations that US interest rates will remain higher for longer, or could even rise further if inflation accelerates, especially with the continued increase in energy prices, are contributing to inflationary pressures. The Relative Strength Index (RSI) currently stands near 77, placing the pair in overbought territory and indicating strong positive momentum for the USD/DKK pair. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (in blue) and the signal line (in orange), reinforcing the likelihood of continued positive momentum for the pair.

Micron Technology

Shares of Micron Technology have risen by about 49% since the beginning of this year. Markets are awaiting the company’s fourth-quarter earnings results for last year, scheduled for Wednesday, March 18, 2026. Market expectations indicate earnings of $8.48 per share, compared with $1.56 per share in the previous reading. As for revenues, markets expect them to reach $18.78 billion, compared with $8.05 billion previously. The Relative Strength Index (RSI) currently stands at 57, indicating positive momentum for Micron shares. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (in blue) and the signal line (in orange), suggesting continued positive momentum for the stock.

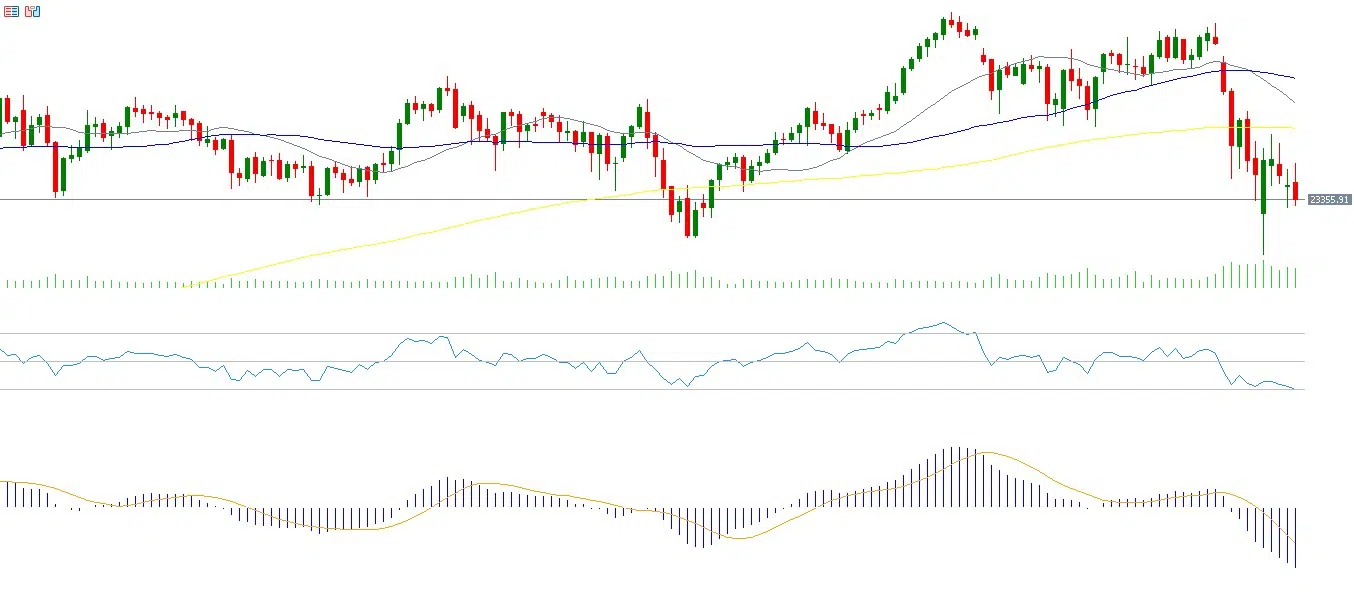

Gold

Gold prices declined for the second consecutive week, closing at $5,019 on Friday, although they remained up about 16% since the beginning of the year. Gold prices have been trading within a horizontal range between $5,000 and $5,200 for more than a week. The strength of the US dollar and the rise in US Treasury yields across different maturities are among the main factors exerting mild pressure on gold prices, in addition to a slowdown in central banks’ pace of gold purchases.

Although expectations that interest rates will remain elevated or rise further tend to negatively impact gold, as it is a non-yielding asset, it is important to remember that gold is also considered a hedge against inflation. Therefore, expectations suggest that upward momentum may continue due to supportive fundamentals such as geopolitical and trade tensions, continued central bank purchases, and rising global debt levels, particularly US debt which has exceeded $38.5 trillion. In addition, investor confidence in public finances has declined, especially at a time when government spending on defense and military activities has increased significantly. This requires financing through the issuance of government bonds, particularly long-term bonds such as 30-year Treasuries, prompting investors to reduce their holdings of these long-term government bonds. The Relative Strength Index (RSI) currently stands at 47, indicating negative momentum. Meanwhile, the MACD indicator shows a bearish crossover between the MACD line (in blue) and the signal line (in orange), indicating negative momentum for gold.

DAX Index

The German DAX index continues its downward trend, declining for the second consecutive week. The index has also erased all its gains for the year and is now down about 4% since the beginning of the year. The main reason behind the decline in European equities is the ongoing geopolitical tensions, particularly the conflict involving the United States and Israel against Iran, along with increasing fears that the conflict could expand amid uncertainty regarding its duration and outcome. This situation may put pressure on high-risk assets, particularly equities.

In addition, the rise in energy prices, including oil and gas, is creating inflationary pressure on the European economy, which could lead to a renewed increase in inflation and may push the European Central Bank to raise interest rates in the coming period. The Relative Strength Index (RSI) currently stands at 36, indicating bearish momentum for the DAX index. Meanwhile, the MACD indicator shows a bearish crossover between the MACD line (in blue) and the signal line (in orange), reinforcing negative momentum for the index.

Key Events This Week

Markets are awaiting several important economic indicators and data releases during this week.

Monday

Markets will monitor retail sales, industrial production, fixed asset investment, and the unemployment rate in China, the Consumer Price Index in Canada, and industrial production in the United States.

Tuesday

Markets will watch the interest rate decision from the Reserve Bank of Australia, with expectations for rates to remain unchanged at 3.85%. Pending home sales data will also be released in the United States.

Wednesday

Attention will turn to interest rate decisions from both the Bank of Canada and the US Federal Reserve, with expectations for rates to remain unchanged at 2.25% in Canada and between 3.50% and 3.75% in the United States. Investors will also closely monitor the tone and remarks of Federal Reserve Chair Jerome Powell regarding the future path of monetary policy. In addition, export and import data will be released in Japan, along with the Consumer Price Index in the Eurozone, as well as producer prices, factory orders, and US crude oil inventories in the United States.

Thursday

Markets will watch the interest rate decision from the Bank of Japan, with expectations for rates to remain unchanged at 0.75%. Investors will also monitor the interest rate decision from the Swiss National Bank, with expectations for rates to remain at 0%. In addition, markets will follow the interest rate decision from the Bank of England, with expectations for rates to remain at 3.75%, and the interest rate decision from the European Central Bank, with expectations for rates to remain at 2.00%. Data on the unemployment rate and employment change in Australia will also be released, alongside industrial production in Japan, income including bonuses and unemployment data in the United Kingdom, average hourly wages in the Eurozone, and US data including the Philadelphia Fed Manufacturing Index, building permits, new home sales, and initial jobless claims.

Friday

Finally, markets will monitor the Loan Prime Rate decision from the People’s Bank of China, the Eurozone trade balance, and retail sales data in Canada.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.