Last week saw the release of a range of mixed global economic data. In the United States, data showed a notable improvement in economic activity as retail sales and both manufacturing and services PMI indices came in above expectations. Meanwhile, the University of Michigan consumer sentiment index came below the previous reading despite exceeding forecasts, and U.S. crude oil inventories rose unexpectedly. In the Eurozone, industrial activity improved as the manufacturing PMI increased, while the services sector entered contraction territory. In the United Kingdom, the unemployment rate declined and retail sales and PMI readings improved, while inflation showed relative stability with a slight increase in the headline index and a decline in core inflation. In Canada, annual inflation rose in March but came below expectations, alongside a slowdown in retail sales growth. Australia also showed improvement in economic activity as both manufacturing and services PMIs returned to expansion territory. In Japan, inflation, exports, and imports increased alongside stronger manufacturing activity, while growth in the services sector slowed. In China, the People’s Bank of China kept its loan prime rates unchanged for the eleventh consecutive month, reflecting continued supportive monetary policy aimed at sustaining economic growth.

Market Analysis

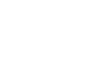

USD/NOK

The USD/NOK pair continues its downward trend, reaching 9.2637 on Thursday, its lowest level since May 5, 2022, declining by around 8% since the beginning of the year before closing on Friday at 9.3176. The pair has fallen by about 11%, effectively entering correction territory, from its peak recorded on March 31, 2026 at 9.8164 to Thursday’s low of 9.2637.

The positive momentum of the Norwegian krone is mainly driven by several factors, most notably the hawkish monetary policy stance of the Norwegian central bank, with interest rates currently at 4.00%. The currency also benefits from interest rate differentials, as Norway’s interest rates are relatively high compared with those of other advanced economies, encouraging carry trade flows. Expectations also indicate that the Norwegian central bank may raise interest rates to between 4.25% and 4.50% by the end of the year, particularly following recent Norwegian economic data that showed the economy remains resilient.

In addition, Norway is one of the world’s largest energy exporters, particularly of oil and gas. As energy prices continue to rise amid the ongoing war and the closure of the Strait of Hormuz, this provides strong support to both the Norwegian economy and the krone.

The Norwegian krone continues to outperform among G10 currencies against the U.S. dollar, ahead of the Australian dollar, New Zealand dollar, Swiss franc, British pound, Canadian dollar, Swedish krona, the euro, and finally the Japanese yen.

The Relative Strength Index (RSI) currently stands at 34, indicating bearish momentum for the pair. Meanwhile, the MACD indicator shows a bearish crossover between the MACD line and the signal line, supporting the continuation of negative momentum for the pair.

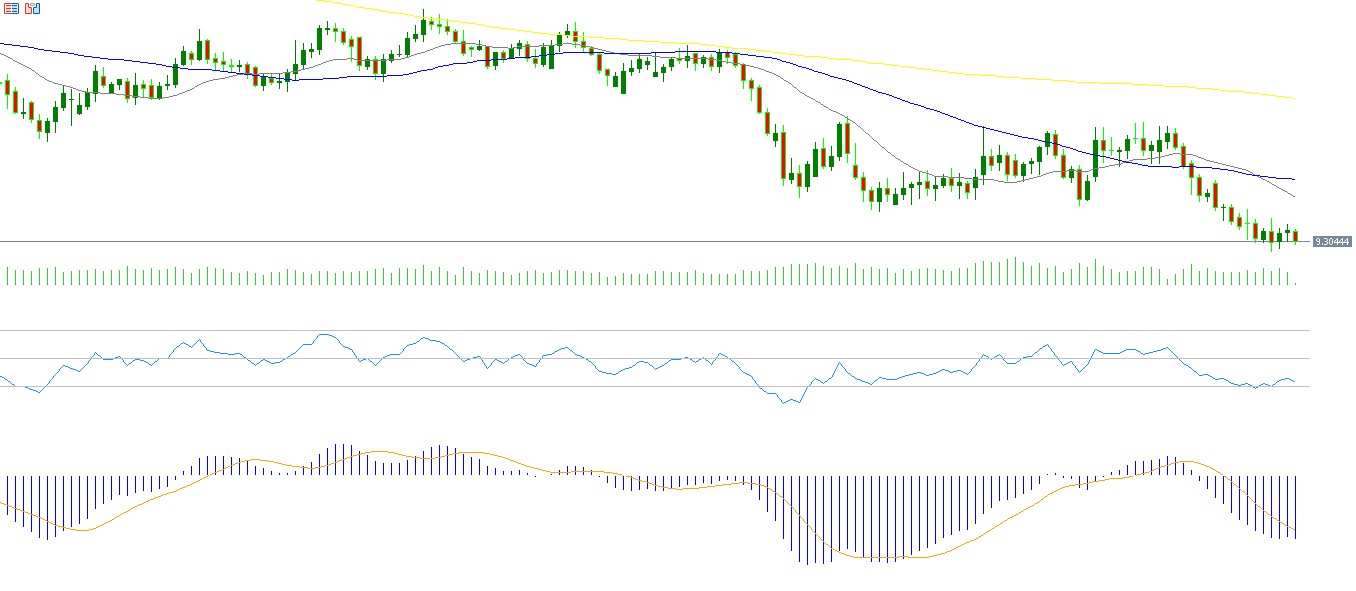

Microsoft

Microsoft’s stock has declined by around 12% since the beginning of the year. Markets are closely watching the company’s earnings results scheduled for Wednesday, April 29, 2026. Expectations indicate earnings of $4.05 per share compared with $3.46 in the previous reading. Revenues are expected to reach $81.30 billion, up from $70.10 billion previously.

The Relative Strength Index (RSI) currently stands at 63, indicating positive momentum for Microsoft shares. Meanwhile, the MACD indicator shows a bullish crossover between the MACD line (blue) and the signal line (orange), suggesting positive momentum for the stock.

Crude Oil

Crude oil prices rose by about 8% last week, reaching $107.40 on Thursday, the highest level since April 7, 2026, before closing near $100 on Friday. Prices have also risen by around 64% since the beginning of the year, outperforming other global financial assets such as equity indices, global bonds, other commodities, the U.S. dollar index, and cryptocurrencies.

The main reason behind this significant rise is the continued uncertainty surrounding geopolitical tensions in the Middle East, in addition to the ongoing closure of the Strait of Hormuz. This has led to the shutdown of 178 global refineries and the U.S. naval blockade on Iranian ports, resulting in continued supply tightness that could push oil prices toward $120, the level recorded in March of this year.

It is also worth noting that during the outbreak of the Russia-Ukraine war, crude oil prices reached $138 per barrel, and expectations suggest that it is not unlikely to see such levels again.

The Relative Strength Index (RSI) is currently around 52, reflecting positive momentum in crude oil prices.

Nasdaq 100 Index

The Nasdaq 100 index rose by about 2.37% last week for the fourth consecutive week, recording a new all-time high at 27,314 points before closing at 27,304 points, up around 8% since the beginning of the year.

It is also notable that the Philadelphia Semiconductor Index reached a new record high on Friday, rising for the eighteenth consecutive session and gaining about 48% since the beginning of the year, reflecting continued strong optimism toward investments in the semiconductor and artificial intelligence sectors.

Expectations indicate that positive momentum in U.S. equities may continue in the coming period despite elevated valuations, mainly due to the strong performance of the U.S. economy, particularly as retail sales and both manufacturing and services PMIs for March exceeded analysts’ expectations, in addition to the strong earnings results reported by most U.S. companies for the first quarter so far.

However, despite this strong optimism, U.S. equity markets face several risks at the current stage, most notably ongoing geopolitical tensions, the closure of the Strait of Hormuz, and concerns related to inflation and fiscal conditions.

From a technical perspective, the Nasdaq 100’s Relative Strength Index currently stands at 85, indicating overbought territory and strong positive momentum. In addition, a bullish crossover between the MACD line and the signal line has appeared, supporting the continuation of this positive momentum. Moreover, a bullish or golden crossover has occurred between the 20-day and 50-day moving averages, which could indicate further upside potential.

Key Events This Week

Markets are awaiting several important economic indicators and events during this week.

On Monday, markets will watch China’s industrial profits data.

On Tuesday, markets await the Bank of Japan’s interest rate decision, with expectations that rates will remain unchanged at 0.75%. The U.S. consumer confidence index will also be released.

On Wednesday, markets will monitor the Bank of Canada’s interest rate decision, with expectations of a hold at 2.25%. The U.S. Federal Reserve will also announce its interest rate decision, with expectations that rates will remain between 3.50% and 3.75%. Attention will be focused on the tone and speech of Federal Reserve Chair Jerome Powell regarding the future path of monetary policy, particularly interest rates. Additionally, Australia’s CPI, Eurozone consumer confidence, U.S. building permits, durable goods orders, the goods trade balance, and U.S. crude oil inventories will be released.

On Thursday, markets await the Bank of England’s interest rate decision, with expectations that rates will remain unchanged at 3.75%. The European Central Bank will also announce its interest rate decision, with expectations that rates will remain around 2.00%. Japan will release retail sales and industrial production data, while China will publish both manufacturing and non-manufacturing PMI readings, along with the Caixin manufacturing PMI. The Eurozone will release GDP, inflation, and unemployment data. In the United States, initial jobless claims and core personal consumption expenditures (PCE) data will also be released.

Finally, on Friday, manufacturing PMI data will be released in Australia, Japan, the United Kingdom, and the United States, alongside Tokyo CPI, Switzerland retail sales, and the ISM manufacturing PMI in the United States.

Please note that this analysis is provided for informational purposes only and should not be considered as investment advice. All trading involves risk.